Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

Remodeling Projects to Avoid When Selling Your Home

It’s common for homeowners to feel compelled to remodel their homes before they sell. Renovating the spaces in your home can increase its value and help you compete with comparable listings in your area. However, some remodeling projects are more beneficial than others as you get ready to hit the market. Always talk to myself or another local agent to determine which projects are most appealing to buyers in your area.

When preparing to sell your home, you want to strike the right balance of upgrades. Making repairs and executing renovations will attract buyer interest, but you don’t want to dump so much cash into remodeling that you won’t be able to recoup those expenses when your home sells.

So, how do you know where to focus your efforts? Your agent is a vital resource in understanding your specific situation—I typically offer guidance to my clients on remodeling efforts that will help sell their home for the best price. Here are a few projects sellers will want to keep off their to-do lists for the best return on investment…

Major, Pricey Upgrades with Long Timelines

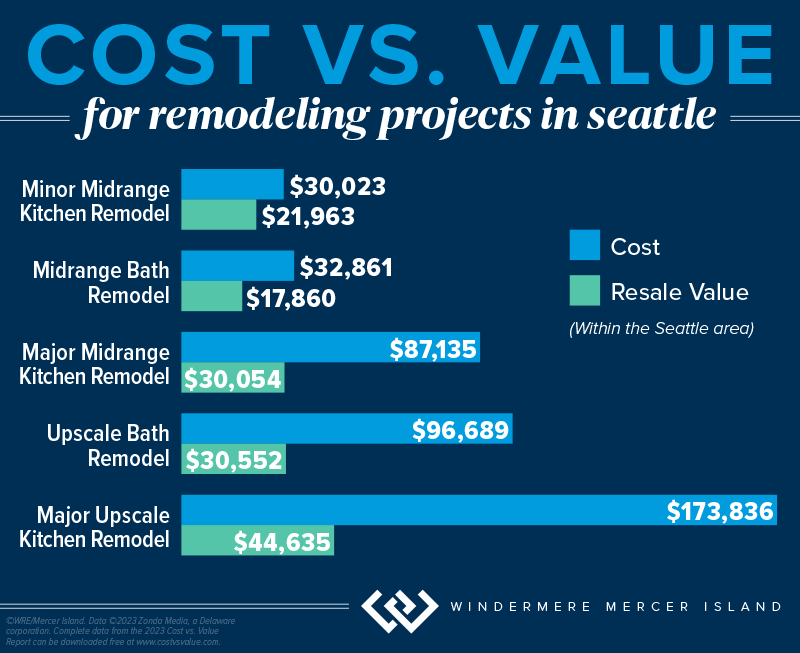

For any remodeling project, an analysis of your home’s value will be key to helping you determine its risk/reward potential (reach out if you’d like one for your home). This dynamic is especially important for big remodels and home upgrades, due to their higher costs. The latest Remodeling Cost vs. Value Report (www.costvsvalue.com)1 data for the Seattle area shows a generally negative return on investment for major, upscale remodeling projects—they only recouped about 25%-30% of their cost…

These projects come with hefty price tags and longer timelines than minor repairs and upgrades, which can complicate factors as you prepare to sell, especially if you have a deadline to get into your new home. They have the potential to temporarily displace you from the property, meaning you and your household may have to find somewhere else to stay until the project is complete.

The Bottom Line: To go through with a major home upgrade before you sell, its schedule must fit with your moving timeline. It should also align with buyer interest in your local market. If the project doesn’t meet these criteria, it should be avoided.

Non-Permitted Projects & Building Code Violations

Before you decide to finish out the basement or make changes to your home’s wiring/structure/mechanical systems, it is important to make sure you obtain the proper city, county and/or state permits + inspections. Non-permitted square footage does not reflect on the county tax record and can lead to low appraisals when the buyer tries to get a loan. Obtaining permits also helps ensure your alterations meet the current building code—otherwise, you may face legal exposure should they create a safety hazard. Furthermore, any non-permitted remodels must be disclosed to the buyer on your Form 17 if you live in Washington State. The buyer’s mortgage lender may also have stipulations saying that the loan may not be used to purchase a home with certain features that aren’t up to code, which could lead to them backing out of the deal.

If you’re selling an older home, you’re not obligated to update every feature that may be out of code to fit modern standards. These projects are often structural and require a significant investment. If the violation in question was built to code according to the regulations at the time, then a grandfather clause typically applies. However, you’ll need to disclose these features to the buyer.

Trendy Makeovers and Upgrades

Lastly, it’s best to avoid remodeling projects that target a specific trend in home design. Trends come and go. Timeless design is a hallmark of marketable homes because it appeals to the widest possible pool of buyers. Keep this in mind when staging your home as well. Creating an environment that’s universally appealing and depersonalized allows buyers to more easily imagine the home as their own.

Wondering which remodeling projects might help your home sell? Reach out any time…I’m never too busy to discuss your options and offer advice based on the current market.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2024, Windermere Real Estate/Mercer Island.

1©2023 Zonda Media, a Delaware corporation. Complete data from the 2023 Cost vs. Value Report can be downloaded free at www.costvsvalue.com.

Adapted from an article that originally appeared on the Windermere Blog, written by: Sandy Dodge.

Tax Benefits Every Homeowner Should Know About

It’s tax season again, but being a homeowner might just make it rain at refund time. Check out the tax-deductible expenses, exemptions, and credits below. Whether you own a house, condo, or mobile home, they can save you big money when you file. Just be sure to compare your total itemized deductions against the standard deduction and see which is higher (you’ll have to choose between standard OR itemized on your return). It’s also good to know what you can’t deduct before you land in hot water with the IRS…

Mortgage Interest

A house payment is comprised of two parts: principal and interest. The principal goes toward reducing the amount you owe on your loan and is not deductible. However, the interest you pay is deductible as an itemized expense on your tax return. You can generally deduct interest on the first $750,000 of your mortgage (or $375,000 each if you’re married filing separately) if you purchased your home after December 15th 2017. Those who purchased earlier (10/14/1987 – 12/15/2017) can deduct interest paid on up to a $1m mortgage.

Property Taxes

You can deduct up to $10,000 of property taxes you paid (or $5,000 if you’re married filing separately). If you have a mortgage, the amount you paid in taxes will be included on the same annual lender statement that shows your loan interest information. If you paid the property taxes yourself but don’t have receipts, you should be able to locate the total tax amount on your county assessor’s website.

Home Improvements

Making improvements on a home can help you reduce your taxes in a few possible ways:

- If using a home equity loan or other loan secured by a home to finance home improvements, these loans will qualify for the same mortgage interest deductions as the main mortgage. Only the interest associated with the first $100,000 is deductible (and if you’ve already maxed out the interest deduction on your main mortgage, you won’t be eligible for any additional deduction for this loan).

- Tracking home improvements can help when the time comes to sell. If a home sells for more than it was purchased for, that extra money is considered taxable income. However, you are allowed to add capital improvements to the cost/tax basis of your home thereby reducing the amount of taxable income from the sale. Keep in mind that most taxpayers are exempted from paying taxes on the first $250,000 (for single filers) and $500,000 (for joint filers) of gains.

- Home improvements made to accommodate a person with a disability (yourself, your spouse, or your dependents who live with you) may be deductible as medical expenses. Examples include adding ramps, widening doorways/hallways, installing handrails or grab bars, lowering kitchen cabinets, or other modifications to provide wheelchair access.

- If you live in Washington State and apply with your county prior to construction, you may be able to get a 3-year property tax exemption for major home improvements (including an ADU or DADU) that add up to 30% of the original home’s value.

Home Office Deduction

If you run a business out of your home, you can take a deduction for the room or space used exclusively for work as your principal place of business. This includes working from a garage, as well as a typical office space. Unlike most of the other deductible expenses, you can deduct home office expenses even if you opt to take the standard deduction.

This deduction can include expenses like mortgage interest, insurance, utilities, and repairs, and is calculated based on “the percentage of your home devoted to business use,” according to the IRS.

Home Energy Tax Credits

For homeowners looking to make their primary home a little greener, either the Energy Efficient Home Improvement Credit or the Residential Energy Clean Property Credit can help offset the cost of energy efficiency improvements. Even better, these are credits, which means they directly lower your tax bill.

- Energy Efficient Home Improvement Credit: 30% of the cost for qualified high-efficiency doors, window, insulation, air conditioners, water heaters, furnaces, heat pumps, etc. Maximum credit of $1,200 (heat pumps, biomass stoves and boilers have separate max of $2,000).

- Residential Clean Energy Credit: 30% of the cost for adding qualified solar/wind/geothermal power generation, solar water heaters, fuel cells, and battery storage.

What You Can’t Deduct:

- Mortgage Insurance (this is a change as of 2022)

- Title Insurance

- Closing Costs

- Loan Origination Points

- Down Payment

- Lost Earnest Money

- Homeowner’s Dues*

- Homeowner’s/Fire Insurance*

- Utilities*

- Depreciation*

- Domestic staff or services*

*Unless it’s related to your home-office deduction—contact your tax pro to see if it’s a qualified deduction for you.

Do you have a low-income, disabled or senior homeowner in your life? Check out this article on King County property tax relief.

Psst…every homeowner’s financial situation is different, so please consult with a tax professional regarding your individual tax liability.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2024, Windermere Real Estate/Mercer Island.

Adapted from an article that originally appeared on the Windermere Blog, written by: Chad Basinger.

7 Simple Ways to Boost Your Curb Appeal

When it comes time to sell your home, first impressions are crucial. Improving your curb appeal will catch buyers’ attention and go a long way toward selling quickly and for the best price. Here are seven affordable changes you can make that have a big impact…

1. Lush Up Your Lawn

A healthy, well-tended lawn will make your home look even more impressive when you start hosting open houses. Clean up all weeds, leaves, and debris, and consistently water to give it that fresh green look. Mow regularly, but not too short or you’ll damage the grass and invite weeds (experts recommend a minimum 3″ height for the Pacific NW). Consider a nitrate-rich fertilizer to keep the grass extra lush and green.

2. Refresh Your Door

Your front door is an opportunity to make a tasteful statement. Look at bold color choices that are within or slightly stretch your home’s exterior color palette. Take time to prepare the surface for a fresh coat of paint to make the color pop as much as possible and try stylish doorknob options that accentuate the aesthetic to give your door some added flair.

3. Update Your House Numbers

New and stylish house numbers are an easy, eye-catching addition to how your home is perceived by buyers. Look for styles that match with your exterior color palette and any exterior lighting fixtures.

4. Plant Colorfully

Adding colorful variety to your front yard will grab buyers’ attention. Align smaller plants like ground cover and flowers neatly within your flower beds, aiming for symmetry when possible. Use larger plants and trees to frame in your entryway or walkup. If your front yard doesn’t have flower beds, try adding hanging planters or window boxes. Because you’ll be competing against nearby listings, it’s landscaping projects like these that can make all the difference in your listing photos.

5. Upgrade Your Lighting

Adding landscape lighting will boost your curb appeal during nighttime, accentuate your shrubbery, and add a welcoming touch for potential buyers, lighting the way to your door.

While we’re on the subject, make sure your house lights are functional. Consider replacing dated fixtures with stylish new versions. Features like automatic dawn-to-dusk sensors will also come in handy if the home will be vacant while it’s listed.

6. Power Wash

Pressure washing your walkways and driveways can instantly improve your curb appeal. If buying a pressure washer is outside your budget, explore rental options from hardware stores in your area.

7. Add an Inviting Touch

Incorporating classic front porch elements like a porch swing, sitting bench, and other outdoor furniture gives a welcoming aura to your home’s entry and creates a sense of comfort for prospective buyers.

Adapted from an article that originally appeared on the Windermere blog April 19th, 2023. Written by: Sandy Dodge.

© Copyright 2023, Windermere Real Estate/Mercer Island.

Buying a Home: A Start-to-Finish Guide

You want to buy a home.

Where do you begin?

When you’re ready to buy—or maybe just ready to start seriously thinking about it—there’s a lot you can do to prepare. Here is a checklist to help you get started…

1. Determine a Price Range

Step one is finding out your budget for your new home. The best way to do that is to meet with a mortgage professional who will review your income, assets, and credit history in order to pre-approve you for a loan. Not only does getting pre-approved allow you to narrow your home search, but it also makes your offer stronger when it comes time buy. If you don’t currently have a mortgage professional, I would be happy to recommend one.

You can also use my Home Monthly Payment Calculator to experiment with different principal amounts, interest rates, down payments, taxes, and insurance to get an idea of what you can afford. Keep in mind that these calculations are meant to be estimates—interest rates change weekly and will be determined by your credit score.

2. Make a Wish List

Imagine your ideal home. How many beds/baths does it have? How big is the backyard? How close is it to the local park? Use our Wish List to guide you in your search online and with me.

3. Start Your Searching

Once you know how much you can afford and what you’re looking for in a home, it’s time to start your search. My online search tool makes it easy to search for homes, keep track of your favorites and subscribe to property alerts when a fitting listing hits the market in your area. I can also send you potential homes and take you to tour them in person once you’re ready to get serious.

4. Know What to Avoid

As you prepare to buy, knowing what not to do can often be just as helpful as knowing what to do. By understanding the pitfalls buyers can fall into, you can identify the signs of these common buying mistakes ahead of time. Check out this article on buying homes that have been flipped, too.

You’ve found the home.

What now?

Once you’ve found the home you can see yourself living in, what’s next? There are many steps to go through before you can officially call yourself a homeowner. I will guide you through this process, but in the meantime, here’s a preview of what you can expect.

1. Negotiation

When making an offer on a home, I will negotiate on your behalf in order to attain the best terms for you. This can include negotiating the price, repair costs, timelines, and contingencies.

2. Purchase & Sale Agreement (Contract)

This is the legal contract you and the seller will enter into once your offer has been accepted by the seller. It outlines the terms and conditions of the sale and is signed by both parties.

3. Inspection

Once the Purchase and Sale Agreement is signed, a home inspector is hired to examine the home’s health, safety, and major mechanical systems. If any issues arise from an inspection, you may be able to renegotiate.

In a competitive offer situation where you wish to waive your inspection contingency in order to make your offer more appealing, I may advise you to conduct a “pre-inspection”—that is, an inspection that is conducted before you put an offer in on the house.

4. Financing

After your offer is accepted, the next step is to get final loan approval. During this process the lender will decide if they’re willing to approve your mortgage based on things like your creditworthiness and the title history and appraisal of the home you want to buy.

5. Title Report

This is a report for you and your lender detailing the history of the home you’re buying to ensure there are no legal barriers to purchasing it.

6. Escrow

Escrow is an impartial third-party process in which documents and funds are deposited by buyers, sellers, and lenders to facilitate the closing of a transaction. To learn more, read this short guide to understanding escrow.

7. Closing

During this final step of the home buying process, ownership is transferred from the seller to the buyer, closing costs are paid, and several legal documents are prepared and signed, all leading to the closing date. After closing is finalized and recorded and the funds are disbursed, the home is yours!

8. Moving Day!

Check out my printable Moving Checklist as you get ready for the big day.

© Copyright 2023, Windermere Real Estate/Mercer Island.

What is an Adjustable-Rate Mortgage (ARM)?

Securing the most advantageous financing for your situation is an integral part of the success formula of buying a home. After getting pre-approved but once you’ve found the home you’d like to pursue, one of your primary tasks is exploring different loan products to see which best fits your situation. This is the fork in the road where you’ll need to decide between a fixed-rate mortgage and an adjustable-rate mortgage (ARM). The following information will help you gain a better understanding of ARMs to help you decide whether they’re right for you.

What Is an Adjustable-Rate Mortgage (ARM)?

After your down payment, your mortgage will finance the remainder of your home purchase. Whereas fixed-rate mortgages allow you to lock in a specific interest rate and payment for the life of your loan, adjustable-rate mortgages’ interest rates will fluctuate over time, thus changing your loan payment. It’s typical for ARMs to begin with a low introductory interest rate, but once that first stage of the loan has passed, they will begin to shift up and down. ARMs generally have a cap that specifies the maximum rate that can occur for that loan.

Let’s say you secure an adjustable-rate mortgage with 30-year terms, the first five of which are at a fixed rate. When the variable interest portion of the loan kicks in, your mortgage’s fluctuations will be measured against an index. If the index is higher than when you secured the loan, your rate and loan payment will go up—and vice versa. How often your ARM rates change depends on your agreement with your lender. Talk to your mortgage broker to learn more about the characteristics of adjustable-rate mortgages.

Pros and Cons of an Adjustable-Rate Mortgage (ARM)

| Pros | Cons |

|

|

|

|

|

|

|

Different Types of Adjustable-Rate Mortgages (ARMs)

Hybrid ARM: As outlined above, a hybrid ARM begins with a fixed-rate introductory period followed by an adjustable-rate period. Typically, a hybrid ARM’s fixed-rate period lasts anywhere between three to 10 years, and its rates adjust at an agreed-upon frequency during the adjustable-rate period, such as once every six months or once a year.

Interest-Only ARM: With an interest-only ARM, you pay just the interest on the loan for a specified introductory period, then the principal payments kick in on top. The longer the introductory period, the higher your payments will be when the delayed principal payments enter the equation.

Payment-Option ARM: Not all states allow these loan products because they can get home buyers into hot water quickly if rates increase. They include flexibility to choose your monthly payments with a payment-option ARM, including interest-only payments and minimum payments that don’t cover interest.

Home Monthly Payment Calculator

To get an idea of how your mortgage payment will fit into your budget, use our free Home Monthly Payment Calculator by clicking the button below. With current rates based on national averages and customizable mortgage terms, you can experiment with different values to get an estimate of your monthly payment for any listing price.

Adapted from an article that originally appeared on the Windermere blog September 28, 2022. Written by: Sandy Dodge.

© Copyright 2022, Windermere Real Estate/Mercer Island.

Should You Remodel or Sell Your Home As Is?

Homeowners who are preparing to sell are often faced with a dilemma about whether to remodel or sell their home in its current state. Each approach has its respective advantages and disadvantages. If you decide to remodel your home, it will likely sell for more; but the increased selling price will come at the cost of financing the remodeling projects. If you decide to sell without remodeling, you won’t spend as much money putting your home on the market, but the concern is whether you’re leaving money on the table.

Should I Remodel or Sell My Home As Is?

To answer this question, it’s important to understand the factors that could influence your decision and to work closely with your agent throughout the process.

Cost Analysis: Home Remodel vs. Selling Your Home As Is

Home Remodel

When you remodel your home before selling, you’re basically making a commitment to spend money to make money. So, it’s important to consider the kind of ROI you can expect from different remodeling projects and how much money you’re willing to spend. Start by discussing these questions with your agent. They can provide you with information on what kinds of remodels other sellers in your area are making and the returns they’re seeing as a result of those upgrades. This will help you determine the price of your home once your remodel is complete.

Then, there’s the question of whether you can complete you remodeling projects DIY or if you’ll need to hire a contractor. If hiring a contractor seems expensive, know that those costs come with the assurance that they will perform quality work and that they have the skill required to complete highly technical projects.

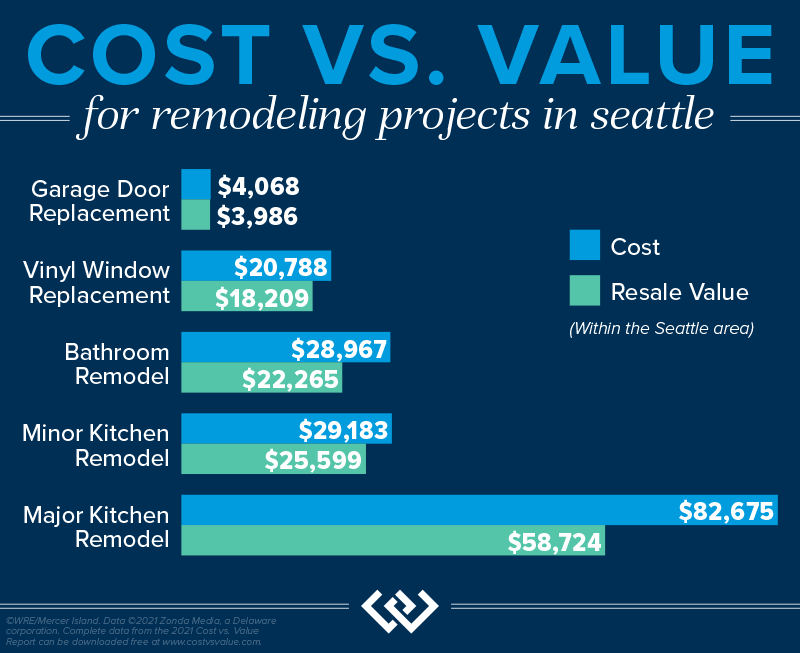

According to the Remodeling 2021 Cost vs. Value Report for Seattle (www.costvsvalue.com1), on average, Seattle-area homeowners paid $28,967 for a midrange bathroom remodel and $29,183 for a minor kitchen remodel, with a 76.9% and 87.7% ROI respectively. This data shows that, for these projects, you can recoup a chunk of your costs, but they may not be the most cost-effective for you. A more budget-friendly approach to upgrading these spaces may look like repainting your kitchen cabinets, swapping out your old kitchen backsplash for a new one, refinishing your bathroom tub, or installing a new showerhead. Other high-ROI remodeling projects may allow you to get more bang for your buck, such as a garage door replacement or installing stone veneer. To appeal to sustainable-minded buyers, consider these 5 Green Upgrades that Increase Your Home Value.

Selling Your Home As Is

Deciding not to remodel your home will come with its own pros and cons. By selling as is, you may sell your home for less, but you also won’t incur the cost and headache of dealing with a remodel. And since you’ve decided to sell, you won’t be able to enjoy the fruits of the remodel, anyway. If you sell your home without remodeling, you may forego the ability to pay down the costs of buying a new home with the extra money you would have made from making those upgrades.

Market Conditions: Home Remodel vs. Selling Your Home As Is

Local market conditions may influence your decision of whether to remodel before selling your home. If you live in a seller’s market, there will be high competition amongst buyers due to a lack of inventory. You may want to capitalize on the status of the market by selling before investing time in a remodel since prices are being driven up, anyway. If you take this approach, you’ll want to strategize with your agent, since your home may lack certain features that buyers can find in comparable listings. In a seller’s market, it is still important to make necessary repairs and to stage your home.

In a buyer’s market, there are more homes on the market than active buyers. If you live in a buyer’s market, you may be more inclined to remodel your home before selling to help it stand out amongst the competition.

Timing: Home Remodel vs. Selling Your Home As Is

Don’t forget that there is a third option: to wait. For all the number crunching and market analysis, it simply may not be the right time to sell your home. Knowing that you’ll sell your home at some point in the future—but not right now—will allow you to plan your remodeling projects with more time on your hands which could make it more financially feasible to complete them.

For more information on how you can prepare to sell your home, connect with one of our local agents—we’re always happy to chat about your situation and offer advice.

1©2021 Zonda Media, a Delaware corporation. Complete data from the 2021 Cost vs. Value Report can be downloaded free at www.costvsvalue.com.

This article originally appeared on the Windermere blog January 10, 2022. Written by: Sandy Dodge.

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative, and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2022, Windermere Real Estate/Mercer Island.

Planning for the Life Expectancy of Your Home

Nothing in life lasts forever – and the same can be said for your home. From the roof to the furnace, every component of your home has a lifespan, so it’s a good idea to know approximately how many years of service you can expect from them. This information can help when buying or selling your home, budgeting for improvements, and deciding between repairing or replacing when problems arise.

According to a National Association of Home Builders (NAHB) study, the average life expectancy of some home components has decreased over the past few decades. (This might explain why you’re on your third washing machine while Grandma still has the same indestructible model you remember from childhood.) But the good news is the lifespan of many other items has actually increased in recent years.

Here’s a look at the average life spans of some common home components (courtesy of NAHB).

APPLIANCES. Of all home components, appliances have the widest variation in life spans. These are averages for all brands and models and may represent the point which replacing is more cost-effective than repairing. Among major appliances, gas ranges have the longest life expectancy, at about 15 years. Electric ranges, standard-size refrigerators, and clothes dryers last about 13 years, while garbage disposals grind away for about 10 years. Dishwashers, microwave ovens, and mini-refrigerators can all be expected to last about nine years. For furnaces, expect a lifespan of about 15 years for electric, 18 for gas, and 20 for oil-burning models. Central air-conditioning systems generally beat the heat for 10 to 15 years.

KITCHEN & BATH. Countertops of wood, tile, and natural stone will last a lifetime, while cultured marble will last about 20 years. The lifespan of laminate countertops depends greatly on the use and can be 20 years or longer. Kitchen faucets generally last about 15 years. An enamel-coated steel sink will last five to 10 years; stainless will last at least 30 years; and slate, granite, soapstone, and copper should endure 100 years or longer. Toilets, on average, can serve at least 50 years (parts such as the wax ring, flush assembly, and seat will likely need replacing), and bathroom faucets tend to last about 20 years.

FLOORING. Natural flooring materials provide longevity as well as beauty: Wood, marble, slate, and granite should all last 100 years or longer, and tile, 74 to 100 years. Laminate products will survive 15 to 25 years, linoleum about 25 years, and vinyl should endure for about 50 years. Carpet will last eight to 10 years on average, depending on use and maintenance.

SIDING, ROOFING, WINDOWS & DECKS. Brick siding normally lasts 100 years or longer, aluminum siding about 80 years, and stucco about 25 years. The lifespan of wood siding varies dramatically – anywhere from 10 to 100 years – depending on the climate and level of maintenance. For roofs, slate or tile will last about 50 years, wood shingles can endure 25 to 30 years, the metal will last about 25 years, and asphalts got you covered for about 20 years. Unclad wood windows will last 30 years or longer, aluminum will last 15 to 20 years, and vinyl windows should keep their seals for 15 to 20 years. Cedar decks average 15-25 years if properly cleaned and treated, while high quality composite decks should easily last 30 years with minimal maintenance.

Of course, none of these averages matter if you have a roof that was improperly installed or a dishwasher that was a lemon right off the assembly line. In these cases, early replacement may be the best choice. Conversely, many household components will last longer than you need them to, as we often replace fully functional items for cosmetic reasons, out of a desire for more modern features, or as a part of a quest to be more energy efficient.

Are extended warranties warranted?

Extended warranties, also known as service contracts or service agreements, are sold for all types of household items, from appliances to electronics. They cover service calls and repairs for a specified time beyond the manufacturer’s standard warranty. Essentially, warranty providers (manufacturers, retailers, and outside companies) are betting that a product will be problem-free in the first years of operation, while the consumer who purchases a warranty is betting against reliability.

Warranty providers make a lot of money on extended warranties, and Consumers Union, which publishes Consumer Reports, advises against purchasing them. You will have to consider whether the cost is worth it to you; for some, it brings a much-needed peace of mind when making such a large purchase. Also, consider if it the cost outweighs the value of the item; in some cases, it may be less expensive to just replace a broken appliance than pay for insurance or a warranty.

ABOUT WINDERMERE MERCER ISLAND

We earn the trust and loyalty of our brokers and clients by doing real estate exceptionally well. The leader in our market, we deliver client-focused service in an authentic, collaborative and transparent manner and with the unmatched knowledge and expertise that comes from decades of experience.

© Copyright 2019, Windermere Real Estate/Mercer Island. Adapted from an article originally posted on Windermere.com.